portability estate tax return

Understanding the portability of the estate tax exemption is crucial to ensuring your spouse has a clear understanding of how portability works. The Tax Relief Unemployment Insurance Reauthorization and Job Creations Act of 2010 introduced for the first time the concept of portability of the federal estate tax exclusion between spouses.

:max_bytes(150000):strip_icc()/ScreenShot2020-02-03at1.41.37PM-322605a2b23a49598d9cdf9faee0a97a.png)

Form 706 United States Estate And Generation Skipping Transfer Tax Return Definition

Which allows surviving spouses including same-sex married couples to claim a carryover of the DSUE amount for any spouse who passed away in 2011 or later.

. To use the DSUE the estate must timely file an Estate Tax Return when the first spouse passes away and the portability election must also be properly completed. Normally an estate tax return is only filed if the decedents estate is valued over the estate tax exemption amount. In order to elect portability of the decedents unused exclusion amount deceased spousal unused exclusion DSUE amount for the benefit of the surviving spouse the estates representative must file an estate tax return Form 706 and the return must be filed timely.

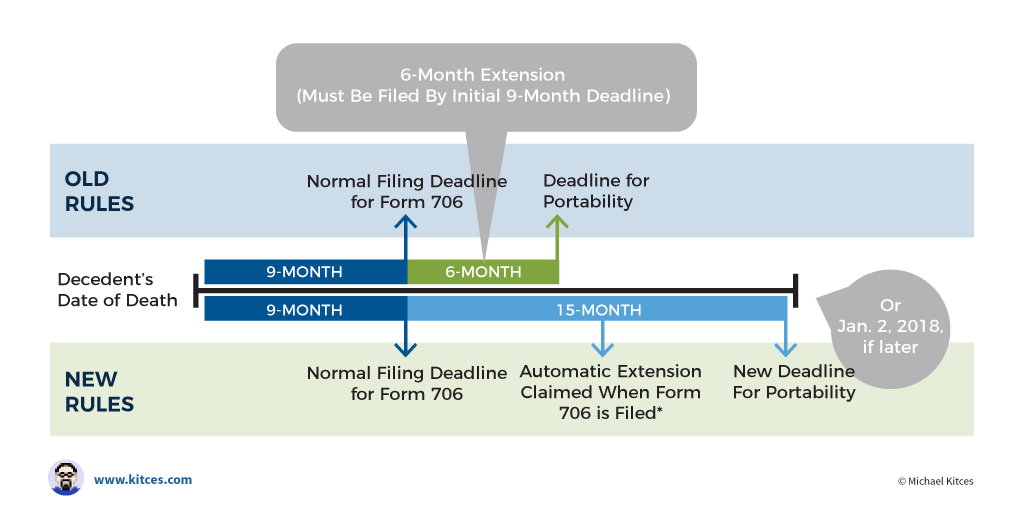

They provided guidance for electing Portability. The due date of the estate tax return is nine months after the decedents date of death however the. In order to use the portability feature an election must be made on the estate tax return of the first spouse to die even if this return would not otherwise be required to be filed.

Estate tax return preparers who prepare a return or claim for refund which reflects. When enacted it was meant to apply only to estates of decedents dying before January 1 2013. A portability election made by a non-appointed executor when there is no appointed executor for that decedents estate can be superseded by a subsequent contrary election made by an appointed executor of that same decedents estate on an estate tax return filed on or before the due date of the return including extensions actually granted.

The due date of the estate tax return is nine months after the decedents date of death however the estates representative may request an extension of time to file the return for up to six months. To claim estate tax portability the estate tax representative must file an estate tax return within 9 months of the first spouses death. Phils 1158 million estate tax exemption was unused and Dora cannot claim the exemption without portability so Dora can only use her exemption of 1158 million when she passes away.

As such if the executor of the estate was required to file Form 706 aside from portability within nine months of the date the decedent passed away including extensions but failed to file the portability election was not allowed. Also on January 2 2013 the American Taxpayer Relief Act ATRA for short was signed. Estate tax return preparers who prepare any return or claim for refund which reflects an understatement of tax liability due to an unreasonable position are subject to a penalty equal to the greater of 1000 or 50 of the income earned or to be earned for the preparation of each such return.

Letss assume the estate tax exemption is still 114 million when Dora dies. The instructions also cover the executors ability to use a checkbox to opt-out of electing Portability of the unused exclusion amount. An automatic six month extension of time to file the return is available to all estates including those filing solely to elect portability by filing Form 4768 on or before the due date of.

Thus the estate tax rate is 40 and Doras estate is still worth 20 million. For any member of a married couple who died after 2010 there is once again an opportunity to file a now very late Form 706 estate tax return to claim portability with a deadline of January 2 nd of 2018. So this is a discussion you can have with the family to make sure they understand the cost and the potential benefits of portability and they can make the right decision of whether or not to make.

These steps could be easily overlooked since an Estate Tax Return does not necessarily have to be filed if the estate is below the exemption amount. Portability allows a surviving spouse the ability to transfer the deceased spouses unused exemption amount DSUEA for estate and gifts taxes to a surviving spouse so long as the Portability election is made on a timely filed federal estate tax return IRS Form 706. Please note these laws being permanent means that they are not set.

Again to elect portability the deceased spouses estate has to file an estate tax return and if that isnt otherwise required that introduces some complexity and some cost into that process. However in order to elect portability an estate tax return must be filed even if the assets are less than the exemption amount. When filing the taxes its important to select the portability election to have the benefits transferred to the surviving spouse.

The key component to portability is the filing of an estate tax return for the first spouse to die. The estate tax is a tax on an individuals right to transfer property upon your death. Thus estates not required to file the Form 706 because the decedents gross estate is below the minimum amount required for an estate tax return to be filed nevertheless must file a.

In 2022 you will be taxed if the total of the gross assets at hand exceeds 1206 million. The IRS has recently revised the instructions to Form 706 United States Estate and Generation-Skipping Transfer Tax Return. Portability allows a surviving spouse the ability to transfer the deceased spouses unused exemption amount DSUEA for estate and gifts taxes to a surviving spouse so long as the Portability election is made on a timely filed federal estate tax return IRS Form 706.

However executors who did not timely file Form 706 and the portability. In order to make the DSUE available to the surviving spouse the Executor of the estate of the first spouse to die must file a federal estate tax return and an make an election for the DSUE to transfer to the surviving spouse even if the estate of the first spouse is under 11400000 and otherwise would not require a federal tax return be filed. If the estate needs more time to file for portability they can apply for a 6-month extension.

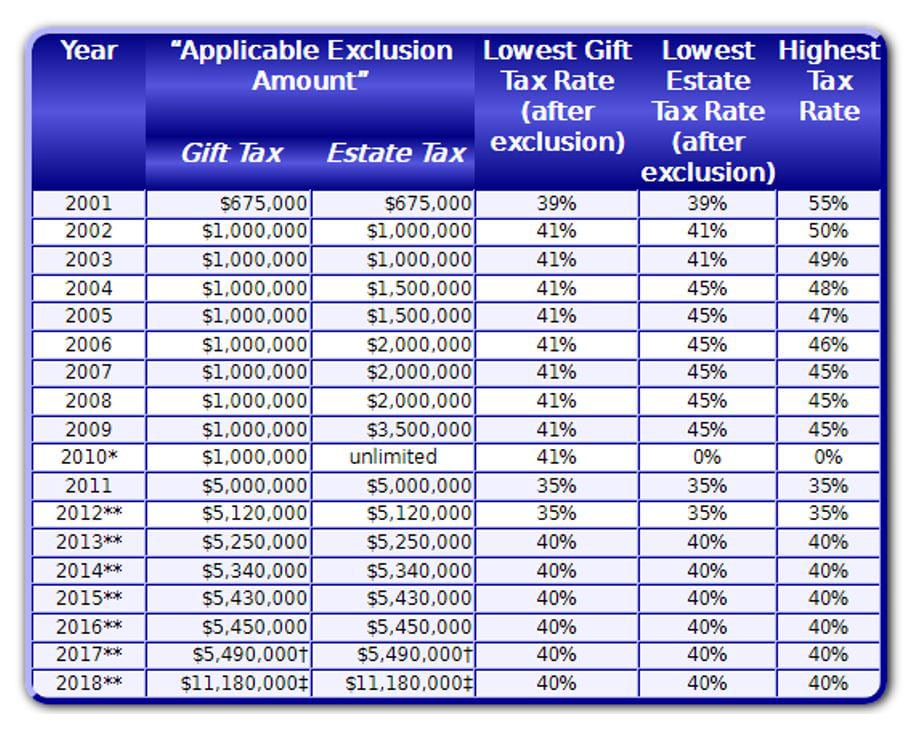

In this case no additional extension is available under the tax code. Aside from increasing the estate tax gift tax and generation-skipping transfer tax exemptions to 5000000 for 2011 and 5120000 for 2012 this law introduced the concept of portability of the federal estate tax exemption between married couples.

File Form 706 Federal Estate Tax Return By Patti Spencer Estategenie Blog

Historical Estate Tax Exemption Amounts And Tax Rates 2022

Is My Estate Subject To Tax Udall Shumway Law Firm Phoenix Az

The New Estate Tax Exemption And Portability Panacea Or Poison

Federal Estate Tax Portability The Pollock Firm Llc

Understanding Qualified Domestic Trusts And Portability

Tax Related Estate Planning Lee Kiefer Park

Locking In A Deceased Spouse S Unused Federal Estate Tax Exemption

Exploring The Estate Tax Part 2 Journal Of Accountancy

Will My Executor Be Required To File An Estate Tax Return Vermillion Law Firm Llc Dallas Estate Planning Attorneys

A New Era In Death And Estate Taxes

Estate Tax Portability Preserving It For The Benefit Of Your Heirs

Chambliss 2014 Estate Planning Seminar Pptx

Estate Tax Exemptions 2020 Fafinski Mark Johnson P A

Portability In Estate Tax Law Special Needs And The Law

Form 706 Extension For Portability Under Rev Proc 2017 34

Estate Tax Introduction Video Taxes Khan Academy

-OCTOBER-27-2021-700x400.jpg)

Federal Estate Tax Return Irs Form 706

What Is Portability For Estate And Gift Tax Portability Of The Estate Tax Exemption The American College Of Trust And Estate Counsel